Personal Finance Basics

The sooner you start, the better off you will be. The second best time to start is now.

Financial advice from the times before covid-19 now seems asinine, outdated, or naive. The prices of most things are skyrocketing. “Save money”?! Who can do that!?

Still, personal finances are the core engine that drive and power many other things in your life. It’s worth mastering the basics and continually practicing to do what you can.

Starting Steps

1. Make A Budget

“You both become and maintain your financial status by budgeting.

The people who don't seem like they need to jog to be fit are the ones that jog regularly.” —The Millionaire Next Door

At the least - start by writing down some categories and track your spending over the course of several months. I used to use YNAB when it was a one-time purchase desktop program. Then they converted to cloud software and it was $4/month. Now it’s $20/month. You’ll have to decide the value of improved clarity and habits.

I've heard positive reviews for Budget with Buckets, ActualBudget (open source), and the Aspire budget spreadsheet, though I haven't tried any.

2. It’s Worth Trying

What I can tell you from my own journey: the change from knowing absolutely nothing about finances to learning, improving, and being in better control of your money is ABSOLUTELY LIFE CHANGING. It has had a huge impact on improving my mental strength, and of course on improving our financial situation.

It’s highly worth buying one year of a budget program if it helps you to build the skills and start. Even if you change to something else later, starting and learning is powerful. If you prefer spreadsheets, physical envelopes, or just manual tracking on paper - power to you.

3. Track your spending

The YNAB docs are well done and motivating - give each of your dollars a “job”. Then track purchases as they happen. Whenever you get some money you ask “What do I need this money to do for me before I get paid again?”. Then give it a job.

Before spending - check your budget. If you don’t have enough, think about your purchase. Is there anything else you could do instead? If you over-spend in one category, shuffle some money around to cover it from something else.

Some people like to automate budget tracking by linking to their bank account online. I prefer to always enter every transaction manually because it keeps me aware. Spending a few minutes each day being aware of your finances and the flow of money is helpful.

4. Break Down Large Expenses

One big insight can be taking large items - like bills you pay once per year - and breaking them down into smaller monthly amounts. It’s easier to plan and budget for $10/month than to suddenly have to find an extra $120.

It’s an amazing feeling when you have a bill arrive and realize: past-you has already budgeted for this, and the money is already there. Just pay it. It’s freeing.

5. It’s Okay To Struggle - Keep Going

Even after years of budgeting I’m still working on the process, and my money doesn’t always balance out. I’m not sure I’ve ever had a ‘normal’ month with no unexpected expenses. That’s okay. YNAB’s attitude of “Roll With The Punches” is fantastic.

Budgeting is not a set-it-once-and-forget-it action - is an ongoing activity. “Be flexible and address overspending as it happens”. You can do it. Don’t worry.

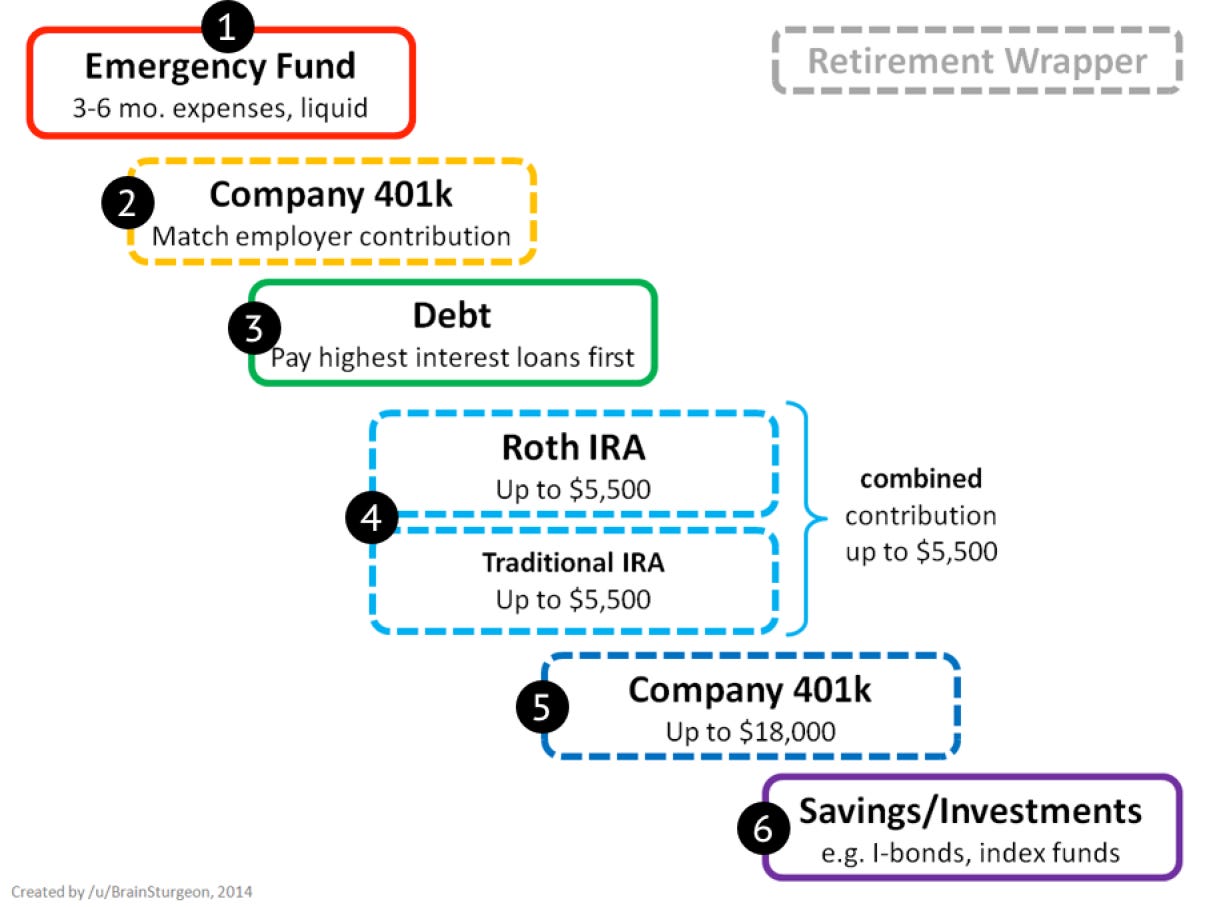

6. Build an emergency fund

Once you have a routine for tracking and planning your spending you should build up some type of emergency fund. An emergency fund is cash you keep on hand to cover up to $1,000 or one month of expenses. This is a shield, to help you deal with unexpected problems and keep making forward progress. It’s cash to protect your plan and your life from the crazy things that are always going to happen. For example - losing your job may be one of the most common emergencies that people face.

Some people will tell you it is bad to keep cash in a bank during times of high inflation, that you are ‘losing money’ compared to investing. An emergency fund is not here to earn you money. An emergency fund is to protect the rest of your life and finances from a sudden emergency.

Building this fund can be a long, tough road. It can take years. But keep at it. Every dollar counts. Starting by putting $10 into an emergency fund is a great step. That’s an extra $10 you didn’t have before!

lcamtuf has some great suggestions in his financial planning section.

Follow The Steps

Once you are able to track and control your monthly income and spending, and you have a buffer of money saved up, then you can move on to further steps. The Personal Finance reddit has a great wiki with information. The important part is to follow the steps *in order*. Build up the important parts first. Step 0 is: Make a budget.

If someone is pressuring you to “INVEST IN THE STOCK MARKET NOW!!”, ignore them. Don’t panic. The point of the steps is to take action in a way that makes sense. If you don’t have an emergency fund yet, you don’t need to be investing in the stock market.

“Every human on the planet has the same two basic financial levers to pull: earn more, or spend less. We recommend both.”

Great Resources

While you are building the habit of budgeting there are a few other great (free) resources you can read to get inspired, learn about growing your income, and get into a strong mindset.

The Millionaire Next Door

"Being frugal is the cornerstone of wealth-building."

A fantastic book that was so good, I bought a (used!) copy and physically put it into the will to gift to my kids (in case I die before I introduce them to it). See if you can find a copy at your local library.

This book preaches:

Live below your means. Be frugal. Don’t spend all of your money.

Allocate your time, money, and energy efficiently, in ways conducive to generating wealth.

Don’t bother with anything flashy or ‘showing off status’. Ignore keeping up with the Joneses.

Be thoughtful and careful in choosing a career that will help you get ahead financially.

This book is a great shift in mindset if you have never been introduced to it. Living frugally below your means is always worth working on.

The Simple Path To Wealth

“The Simple Path To Wealth” by JL Collins is a great book. You can read it online for free at “The Stock Series” .

The summary is:

Once you are ready to invest (i.e. you have a budget and an emergency fund)

Purchase index funds with a low management fee (often named Management Expense Ratio - MER)

Buy more regularly. e.g. a bit every paycheque

Leave them alone until you need money for retirement

I believe that any MER above 0.2 is criminal; avoid it like the plague. If you get locked into a fund with a MER of 1.0 or higher they are stealing huge swaths of your money. Be careful with employer investments that force you into a set of funds - they can have huge MERs of 2.0+.

In my books you want to invest in Vanguard funds and nothing else, because of their philosophy and legal setup of “the investors are the owners”. Accept no grifting substitutes.

Get Rich Slowly - The Moneyboss Manifesto

“The Moneyboss Manifesto” is a free PDF you can read online. The author’s story going from deeply in debt to taking charge of their own finances and making improvements is inspiring. They pitch running your personal finances the same way you would run a business, and working to improve your ‘profit margin’ so you can invest it back into yourself.

The author walks you through creating a personal plan for what you what to do with your life, analyzing your current finances to calculate your monthly ‘profit’ or ‘loss’, and strongly encourages you to work at earning more total money.

“The Moneyboss Manifesto” covers the whole financial journey from scratch to success, so it’s great to walk through and follow along. The author runs getrichslowly.org , which is also a good resource.

The Shockingly Simple Math Behind Early Retirement

Aggressively lower your expenses. Invest the savings.

The goofily named Mister Money Mustache penned this opinionated article in 2012 and became one of the first big writers in the revamped personal finance scene. While you may not succeed in reorganizing your life this drastically, moving in the right direction is still valuable.

Personal Finance For Regular Folks

The essay “Emergency preparedness for regular folks” is worth reading in entirety. Zalewski is a smart, insightful person. But the lists for saving money, keeping what you saved, and dealing with inflation are straightforward and useful.

The “Good And Cheap” Cookbook

A fantastic project where the author collected and created recipes that are affordable by regular people under a budget of SNAP / food stamps. The book has several pages on pantry management and buying in bulk. The entire book has been graciously published under a Creative Commons “Attribution - NonCommercial ShareAlike“ license, meaning anyone can share it and use it for free! You can also buy physical copies.

Avoid Grifters And Fraud

There are many misleading writers who try to convince you they have the answers for personal finance. Ignore Robert Kiyosaki and "Rich Dad, Poor Dad" - he's a fraud peddling illegal advice. I similarly dislike sales-y and pushy blogs like Ramit Sethi because they are all sizzle and no steak. They have little useful advice, but keep stringing you along with the promise that surely they will, someday. If you pay them.

In reality these authors have discovered perhaps the only true way to get rich quickly: selling products to suckers other people promising you will help them get rich.

Avoid Comparing Yourself To Others

It’s worth noting that many people with large financial success stories may have had a leg up in terms of inheriting money, family gifts, or getting very lucky. Don’t stress about comparing yourself to others, or feeling you are ‘falling behind’ or ‘not doing enough’.

Each step you take is good. Your path will be different from anyone else’s. Don’t worry about other people who seem to be faster or doing better - they have their own struggles and failures too.

You’re only competing against your past self, and if you’re trying, learning, and working on it - you are winning. Don’t worry about anyone else.

Ways to Reduce Expenses

Cook food at home and do meal prep, rather than ordering from restaurants.

See how much you can save by planning what meals you make for the whole week.

The book “A New Way To Dinner” is a nice guide for this

Learn how to fix your house and car with DIY and youtube, to save money not calling a repairman.

Plan dates, social get-togethers, and fun family activities that are cheap or free. Go for a picnic, go for a hike, swim in the lake, play a card game.

For any board game I buy, I track the number of times that we actually play it. I don’t buy anything new until I have worked down to a certain “dollars per use”, to get value out of my purchase.

Once each year - do a review of all of your bills - insurance, internet, etc. and get quotes from competitors to see if you can save money. Often switching companies or threatening to switch each year can save you a tiny bit.

The books above have many other tips.

Don’t Get Discouraged

“Net worth does not equal self worth”

—Vicki Robinson, “Your Money Or Your Life”

Improving finances is a marathon, not a sprint. Every little bit helps. If it seems overwhelming - ignore everything, and just focus on one small thing you can do.

In “Your Money Or Your Life” Vicky Robinson cites a study that surveyed thousands of workshop attendees: “No matter how much money anyone at the workshop was making, *every* attendee stated they felt they needed to make about 50% more to feel financially capable and able to make ends meet”. And yet - there they are, attendees in every group, still making ends meet.

So it might always be a journey. Don’t get discouraged. Focus on what you can control and take it one step at a time.

Invest In Yourself

Continually work to practice and improve your own skills, no matter what field, trade, or hobby you are in. Building skills and networking helps you open options and get further ahead.

Other Types Of Wealth

Assets are things that appreciate in value over time. But don’t forget there are other types of wealth:

Your personal health, fitness, and flexibility

Your positive relationships with friends and family

Skills you learn

Community you build

Mental resilience and positive attitude

Food in the pantry

Investing your time and resources in these is also a good investment.

Good luck!

Links

Money

"The Millionaire Next Door”

Online summary, approved by the author

“The Shockingly Simple Math Behind Early Retirement”

Unsure how valid this is post covid-19 price increases

Food

“A New Way To Dinner” - how to plan, shop, and do meal planning

Fixing

HouseImprovments youtube channel. This guy has been working as a tradesman for years, is the real deal, and has many helpful videos.